.png)

We have been speaking about the great wealth transfer for a few years now, when it was first reported that around $60 trillion will move from older generations to younger ones by 2060. Since then, it has always been present in the conversation when talking about trends, insights, or best practices for WM firms or private banks.

The crux of the argument is that, as wealth falls into younger generations’ hands, the demographic expectations shift with it. Whether Gen X, millennials or even the older end of Gen Z, there is a minimum service expectation that relies heavily on digital channels.

Time is running out

Up until now, appealing to new communication preferences has been a problem for the future. Relationship managers and wealth advisors look at their healthy book of business and it is difficult to justify the overhaul of interaction processes and training time necessary to embrace (or enhance) digital transformation.

Now, that time is officially running out.

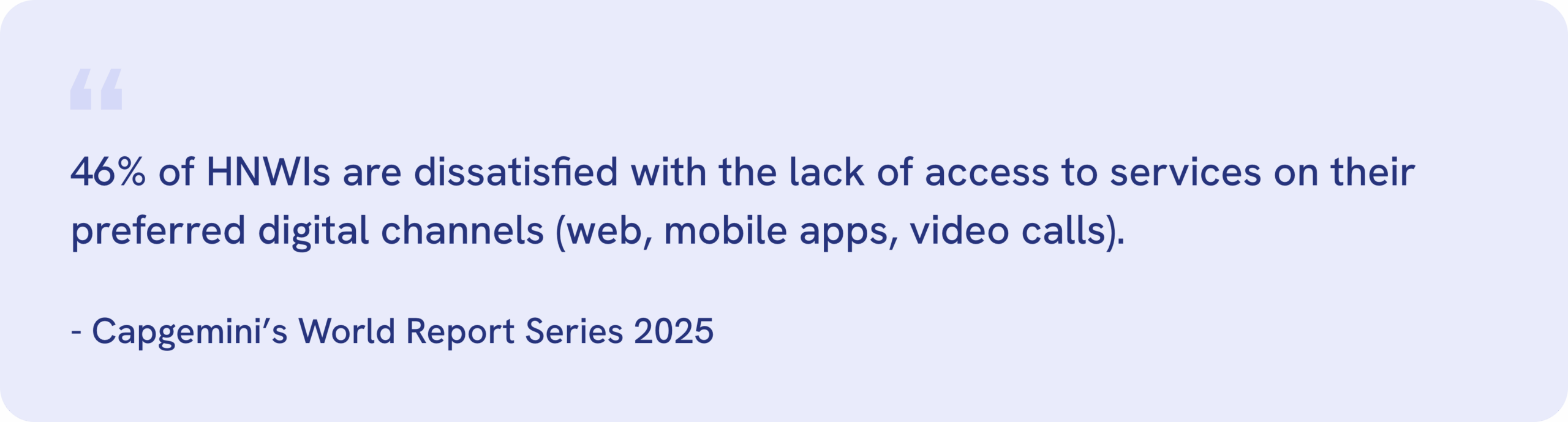

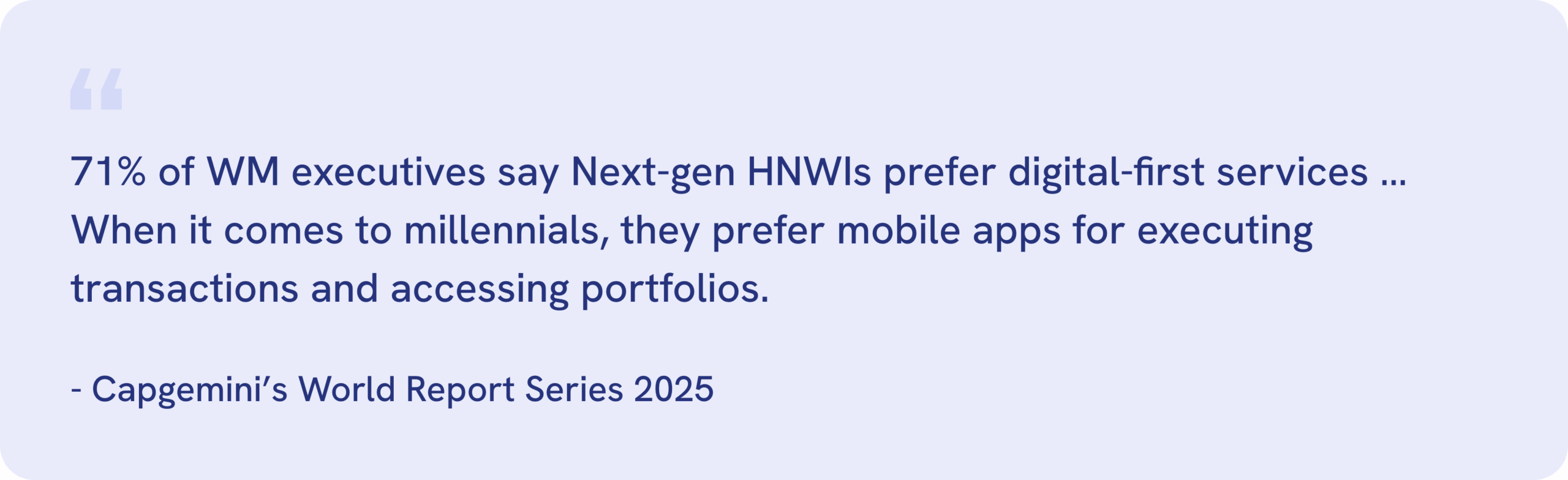

The recent Capgemini’s World Report Series 2025, drawing on surveys from 6,472 HNWIs, 141 wealth management executives, and 1,306 RMs, has produced some alarming findings that point to a watershed moment for WM firms and banks.

We mentioned above that there is a “minimum” service expectation for this demographic. The issue, however, is that this minimum expectation is quite high, involving a wide range of apps, chat channels, interactive experiences and omnichannel convenience. They also look for proactive advisory, a concierge-like service, and cross-functional collaboration with family offices and specialists.

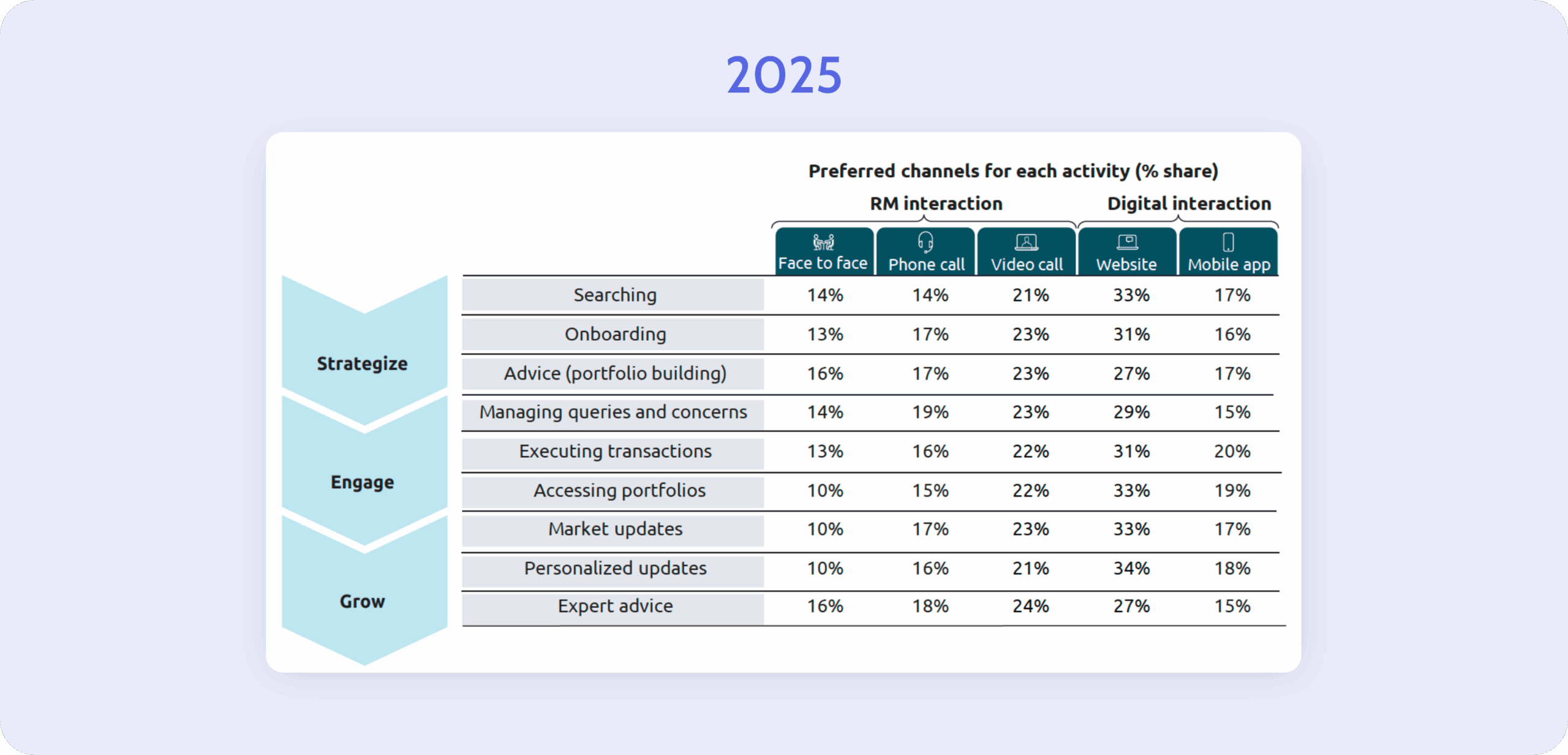

The digital shift visualized

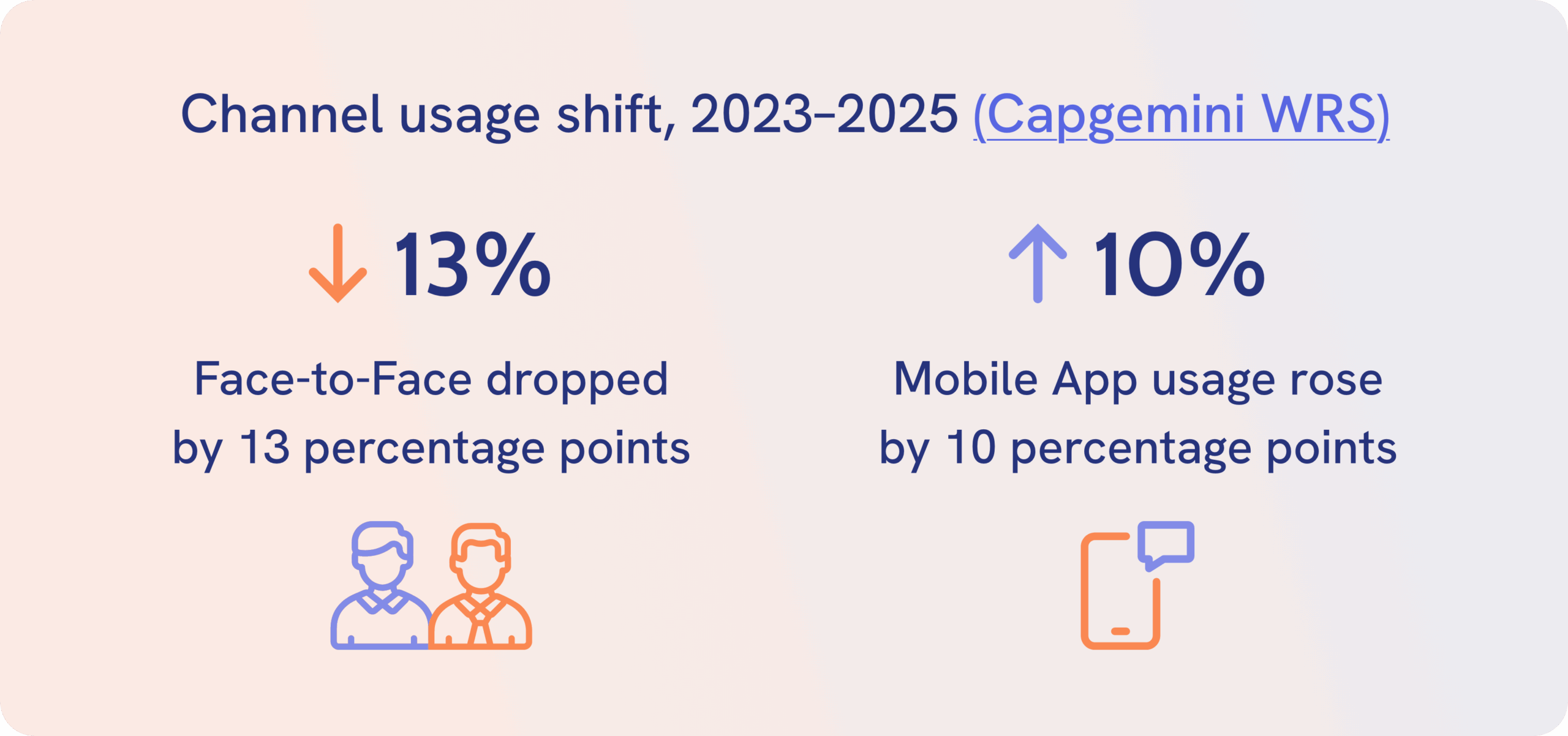

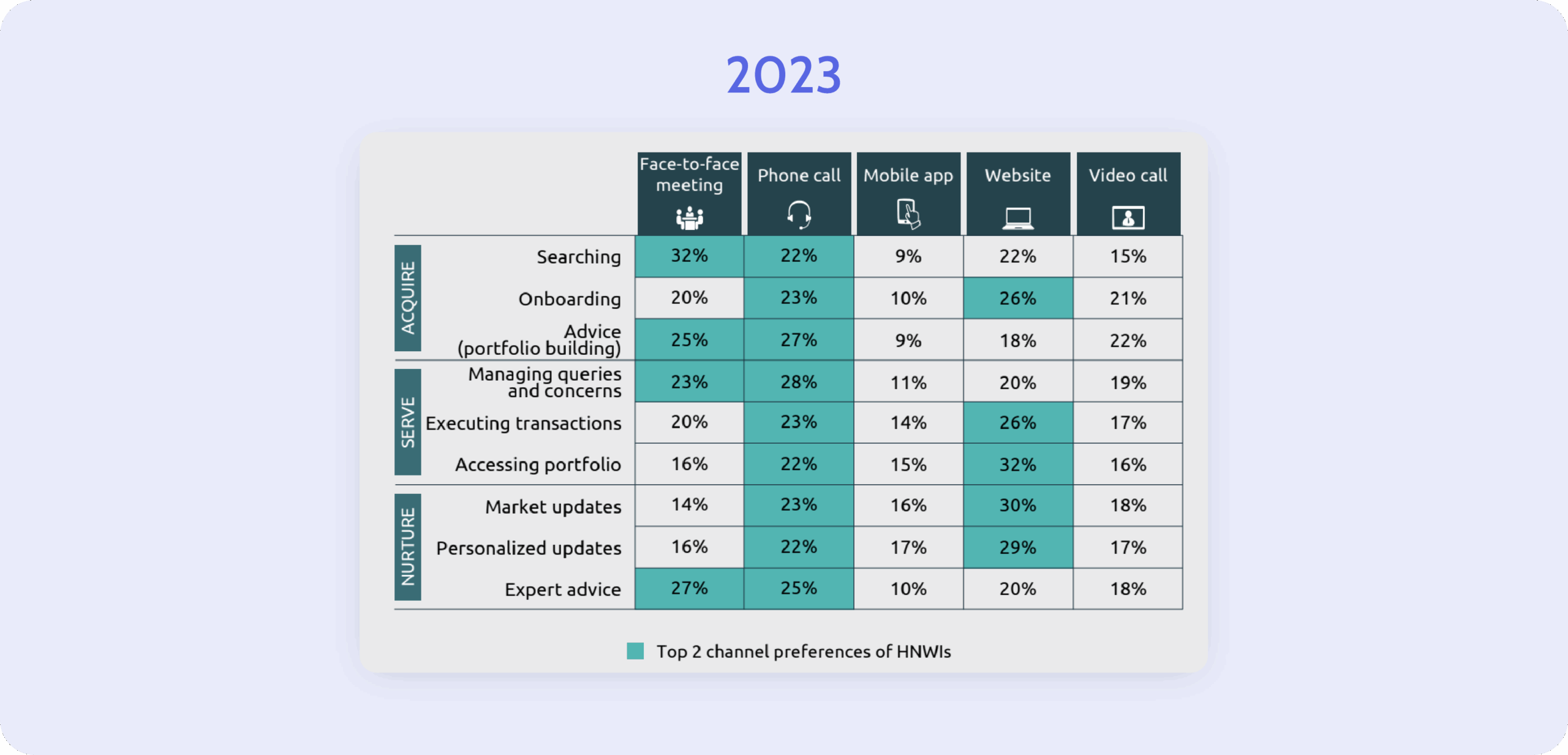

Again, this isn’t a “future problem” but something that we can visually see and measure over just the last few years.

In just two years alone, the shift to digital channels has accelerated drastically. In fact:

And these are just some of the findings. You can see a full comparison below from Capgemini.

The fact of the matter is that, considering how long it takes to implement secure and compliant digital tools in private banking, it is essential to invest today. Beginning in two years means playing catch up on a trend that’s already accelerating.

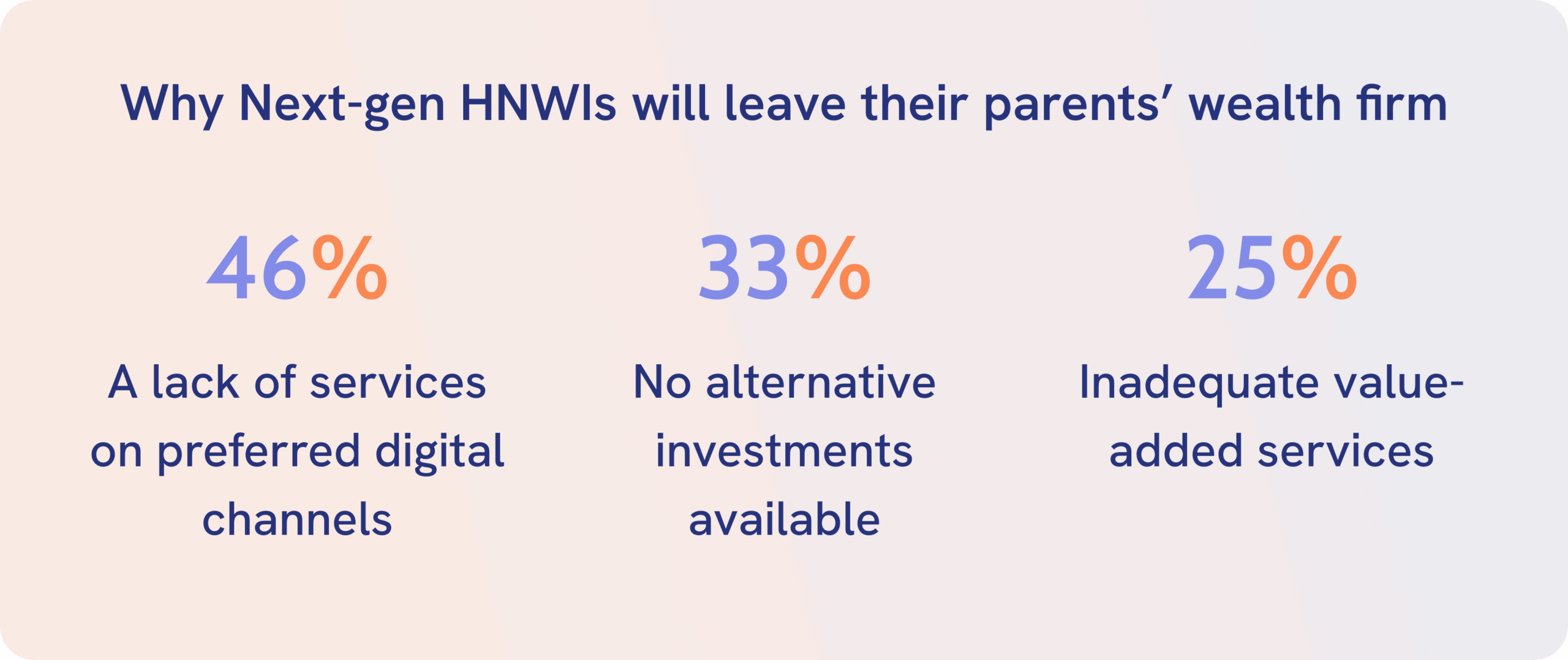

Next-gen HNWIs will leave

For any firms that believe customer loyalty through family ties – or at least churn inertia – will save them are in for a rude awakening. The Capgemini report found that “81% of Next-gen HNWIs plan to switch their parent’s wealth management firm with one one to two years after inheritance.”

The main reasons for this are:

The opportunities are there

With any change comes opportunity for those agile enough to adapt and step up. The Capgemini report identified three strategic approaches that firms and banks must take to maintain or expand their market share.

The findings are:

In this article, we are focusing on the second strategic approach, examining how we can deliver on younger HNWI expectations. If you would like more insights on how to boost engagement through consistent, timely client interactions, you can see our post on the strategic approach here.

Back to the matter at hand, what can firms do to improve value delivery for new HNWIs?

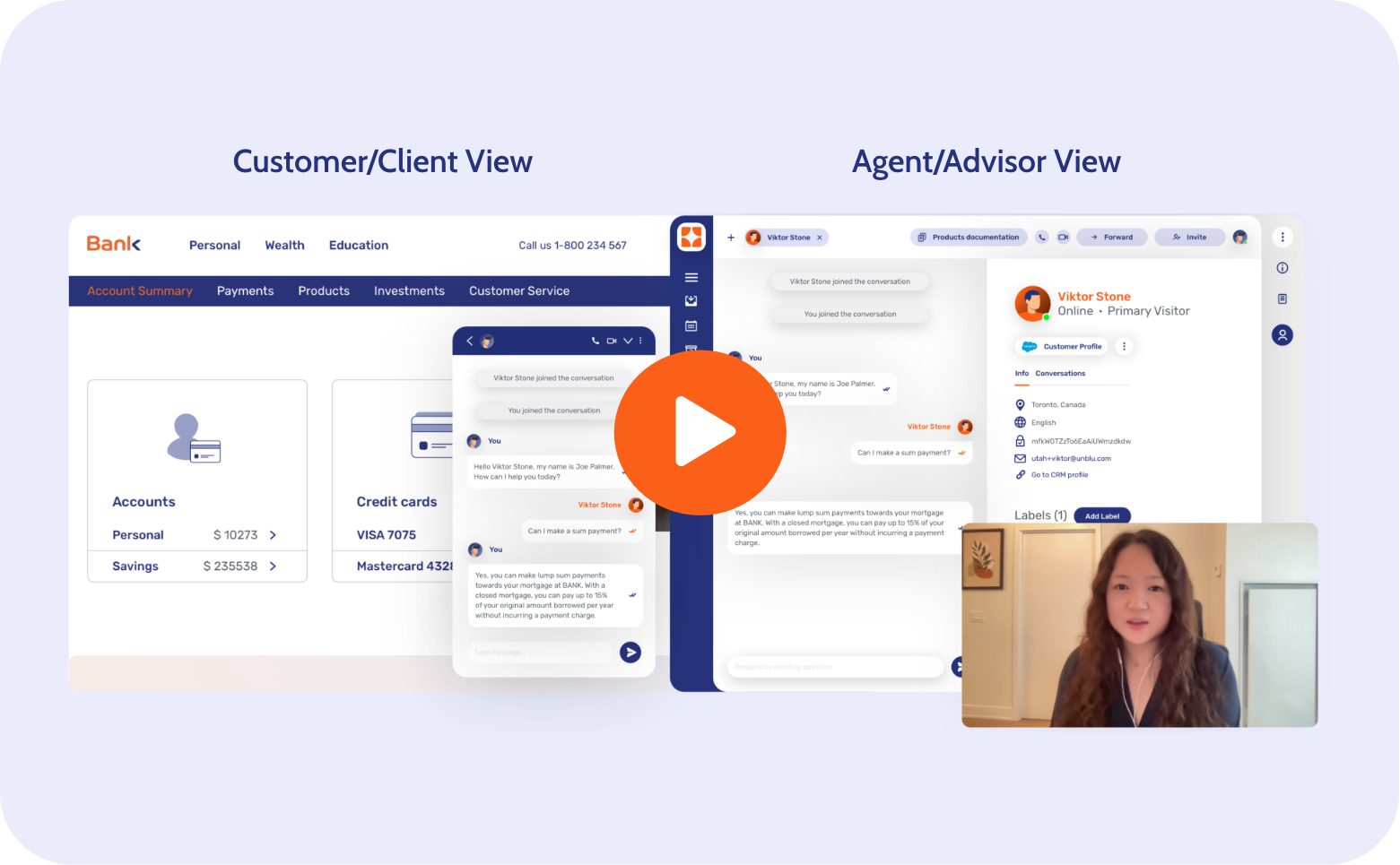

Expanding value delivery for next-gen HNWIs with Unblu

According to client preferences gained from the report, there are a number of channels and capabilities that organizations can implement to improve value delivery.

1. Omnichannel experience

Enable secure engagement via web portal and mobile apps, supporting chat, video, and document sharing across channels.

2. Mobile centric approach

Meet Next-gen clients where they are already active. This means providing a messaging experience that mirrors popular apps and leverages familiar notifications, all while maintaining enterprise-grade security and compliance.

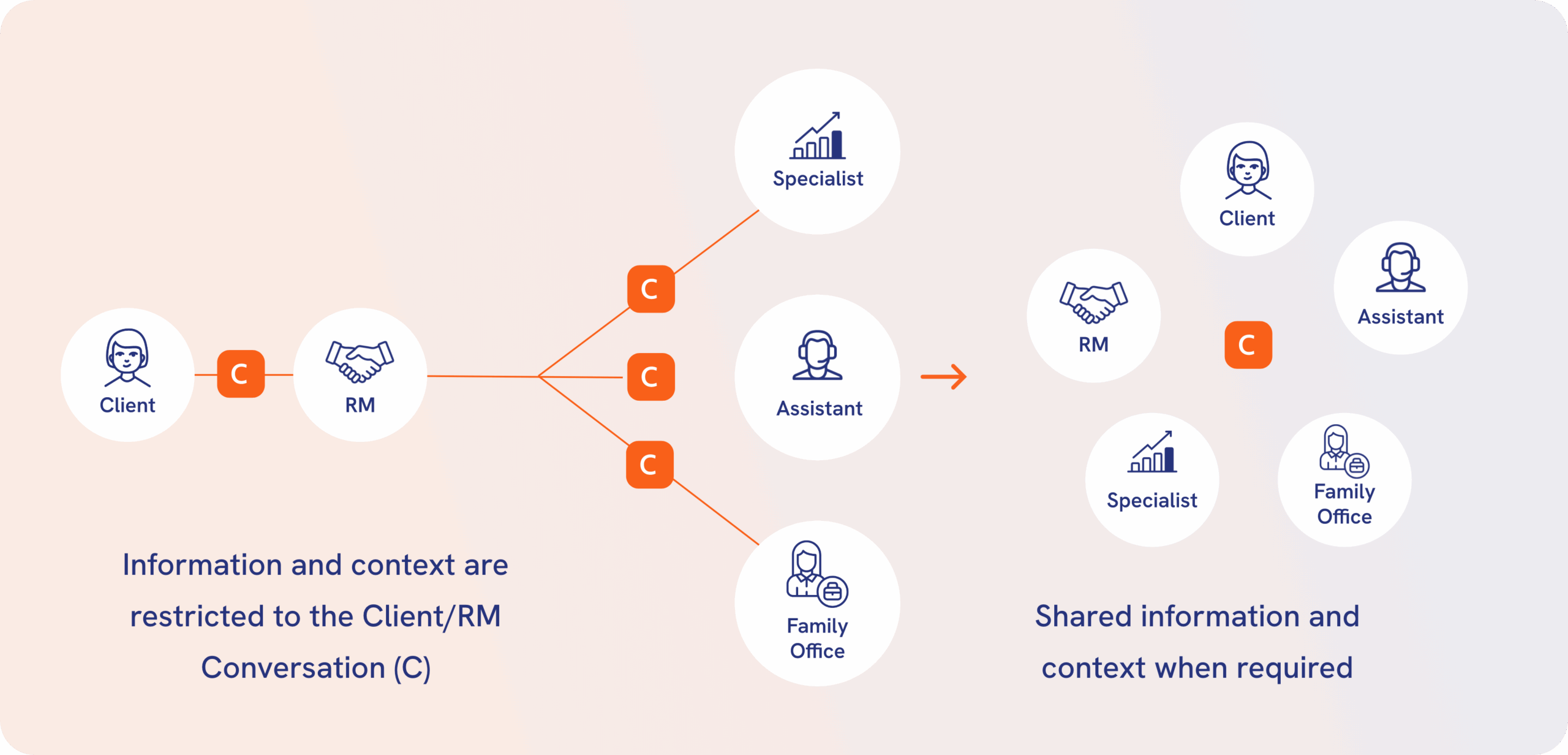

3. Multi-party collaboration

Include family office members, legal or tax advisors, all within one secure conversation.

Find more information on the above capabilities here.

Case study: What does modern value delivery achieve?

At Unblu, we work with some of the largest private banks and wealth management firms.

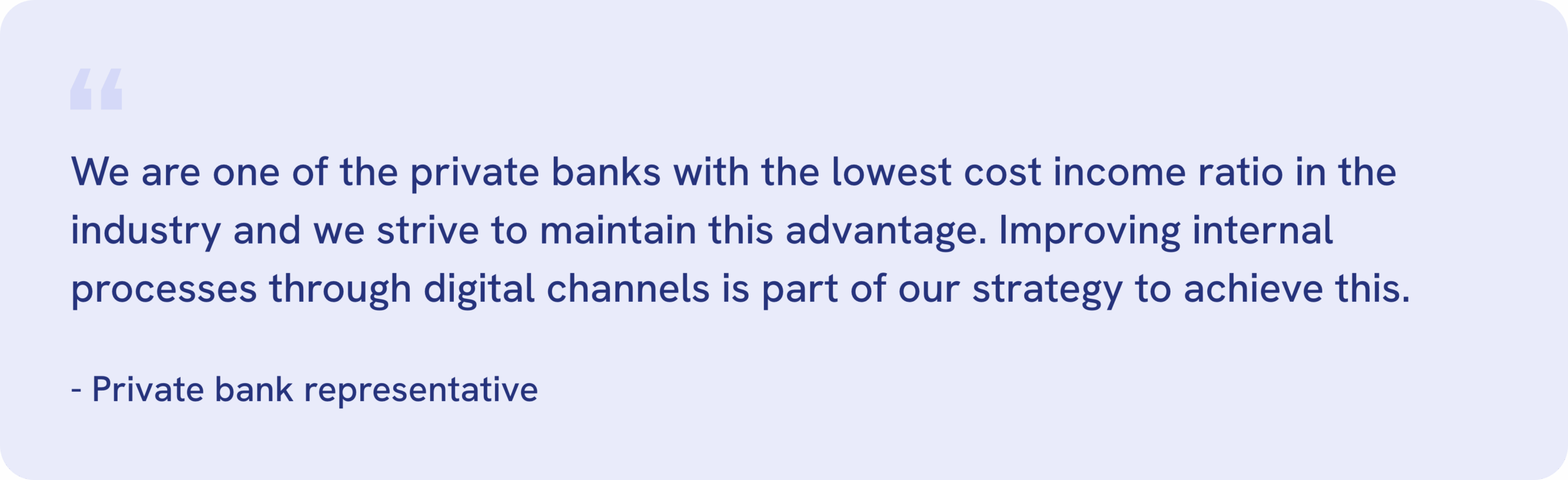

Improving internal processes with digital channels

An Unblu customer, a Swiss private bank with over 180 years of experience, decided it was time to make a change. By partnering with Unbu, they:

- Took steps to remove call-backs, streamlining execution, and freeing up advisor time.

- Equipped 1,000 RMs with Secure Messenger, Video & Voice, and Document Collaboration.

- Ensured all conversations were compliant and secure, with all of them embedded behind e-banking.

- Enabled remote client meetings and ongoing support beyond in-person limitations.

Adopting a mobile-first strategy

Another reputable bank based in the Middle East took steps with Unblu as a customer to adopt a mobile-first strategy and better service their retail, wealth, and corporate client base of over 170,000 account holders.

The steps they took included:

- Deploying chat, Video & Voice, and Mobile Co-Browsing within their mobile app

- Extended Unblu capabilities to Private Banking, reinforcing the app as a single point of client contact

- Enabled appointment scheduling and flexible engagement (video, private meeting, or live chat)

After taking these actions, the bank found overall benefits included enhanced convenience, reduced friction, and a strengthening in client relationships through app-based interaction.

Digital transformation can’t wait

The numbers don’t lie: the great wealth transfer is no longer a distant trend – it’s an unfolding reality. As expectations evolve, so too must the tools, channels, and strategies that define client relationships.

For wealth management firms and private banks, success will depend on their ability to meet clients where they are, on digital channels that offer both convenience and meaningful interaction.

The window to adapt is narrowing. Forward-thinking firms are already aligning their digital strategy with these shifting demands. For everyone else, the question is no longer if change is needed, but how quickly it can happen.

Want to find out more?